Agentic AI in Finance: Moving From Discovery to Autonomous Action

Generative AI was just the warm-up. Discover how Agentic AI is reshaping financial services, creating adaptive experiences, and demanding a new architectural core.

Generative AI was just the warm-up. Discover how Agentic AI is reshaping financial services, creating adaptive experiences, and demanding a new architectural core.

Subscribe now for best practices, research reports, and more.

For the last three years, the financial services industry has been fixated on Generative AI. We successfully deployed chatbots that could summarize policy documents and drafting assistants that sped up marketing copy. This was "Wave 1": the era of AI as an Assistant.

According to a new report from Oliver Wyman, Google, and Innovate Finance, we are now crossing a critical inflection point into "Wave 2." We are entering the era of Agentic AI.

The distinction is profound. While a GenAI assistant can tell you how to apply for a mortgage, an AI Agent can execute the application, verify the documents, negotiate the rate, and coordinate with the conveyancer—autonomously.

For C-Suite leaders, this transition shifts the strategic focus from "efficiency" to "agency." The question is no longer "How can AI help our staff work faster?" It is "How can AI execute complex workflows on behalf of our customers?"

The industry is not adopting this technology uniformly. The report identifies a divergence in strategy between incumbents and fintechs, creating a "Dual Pace" of adoption.

Incumbents are largely deploying AI in the back office. They are using agents to automate KYC refreshes, streamline anti-money laundering (AML) alerts, and generate internal reports. This is a logical starting point given their legacy constraints and regulatory burdens. It drives efficiency but remains invisible to the customer.

Fintechs, leveraging modern, cloud-native stacks, are deploying AI at the front end. They are building "portfolios of one" and dynamic interfaces that adapt in real-time.

This creates a strategic risk for banks. If fintechs monopolize the experience layer with helpful agents while banks only use agents for operations, banks risk becoming invisible utilities highly efficient pipes with no customer relationship.

Transitioning to Agentic AI is not a plug-and-play upgrade. It requires a fundamental re-architecture of the bank. Agents need permissioned access to data, secure rails for execution, and an orchestration layer that can manage multi-step reasoning.

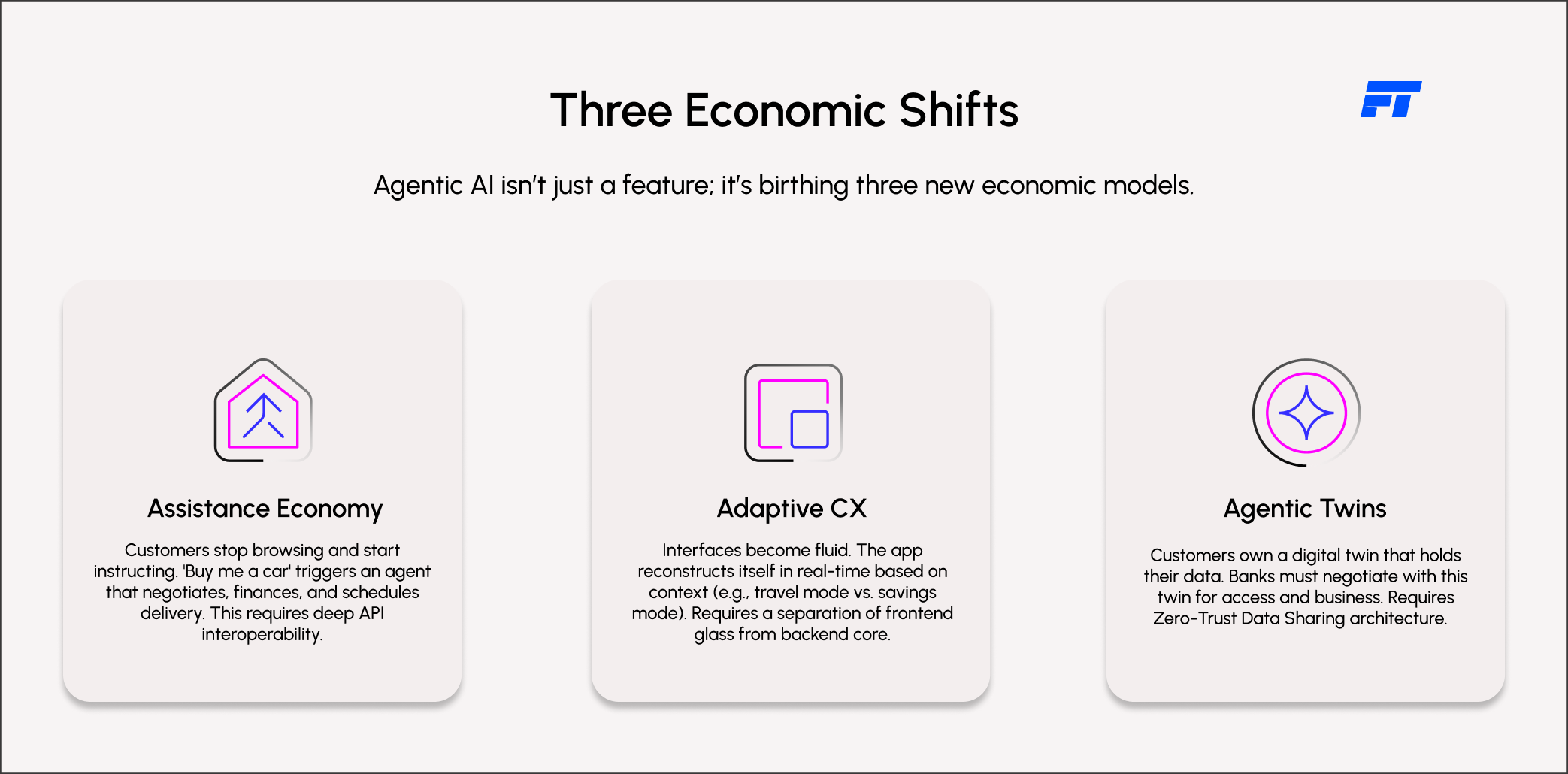

This shift will birth three distinct new economic models within financial services.

In the near future, customers will not browse banking apps; they will instruct agents.Imagine a customer prompting their banking app: "I want to buy a car."

In the current model, the app provides a loan calculator. In the Assistance Economy, an "Auto-Buying Agent" springs into action. It profiles the customer's preferences, scans the market for inventory, negotiates the price with dealerships, optimizes the financing package, and schedules the test drive.

The Architectural Challenge: This requires deep interoperability. Your banking platform must expose APIs that allow internal agents to communicate securely with external third-party services (dealerships, insurers, regulators). If your core is siloed, your agents are blind.

Today, every customer sees roughly the same mobile banking interface. Personalization is limited to a "Welcome, [Name]" banner.

Agentic AI unlocks Adaptive CX. In this model, the interface itself is fluid. It reconstructs itself in real-time based on context.

The Architectural Challenge: This requires a separation of the "glass" (frontend) from the "core" (backend), connected by a high-speed intelligence layer. Monolithic frontend frameworks cannot support this level of dynamism.

Perhaps the most disruptive concept is the Agentic Twin. This is a digital representative owned by the customer not the bank.

This Twin holds the customer's identity, preferences, and financial data. It acts as a gatekeeper. Instead of a bank chasing a customer for data, the bank's agent negotiates with the customer's Twin. The Twin grants permission for specific data access in exchange for value (e.g., a better rate).

The Architectural Challenge: This flips the data ownership model. Banks must build systems designed for Zero-Trust Data Sharing and Verifiable Credentials. You are no longer the custodian of the customer's digital life; you are a service provider applying to be part of it.

Embracing Agentic AI offers tangible returns beyond novelty:

The shift from "Discovery" to "Doing" is the defining challenge of the next five years. The winners will not be the institutions with the best AI models those are commodities. The winners will be the institutions with the best Agentic Architecture.

To compete in the Agentic Economy, you must break down data silos, expose granular APIs, and build a governance framework that allows agents to act with autonomy and safety.

Fyscal Technologies specializes in this transition. We design the vendor-agnostic, API-first architectures that serve as the foundation for Agentic AI. We help you move from a static repository of funds to a dynamic engine of financial action.

Ready to build your Agentic infrastructure?

.png)

.svg)