Stop Losing Revenue to Batch Delays: The Real ROI of Real-Time Ledgers

Discover how real-time ledger systems outperform batch processing on cost, speed, and compliance. Explore the technical shifts reshaping fintech infrastructure.

Discover how real-time ledger systems outperform batch processing on cost, speed, and compliance. Explore the technical shifts reshaping fintech infrastructure.

Subscribe now for best practices, research reports, and more.

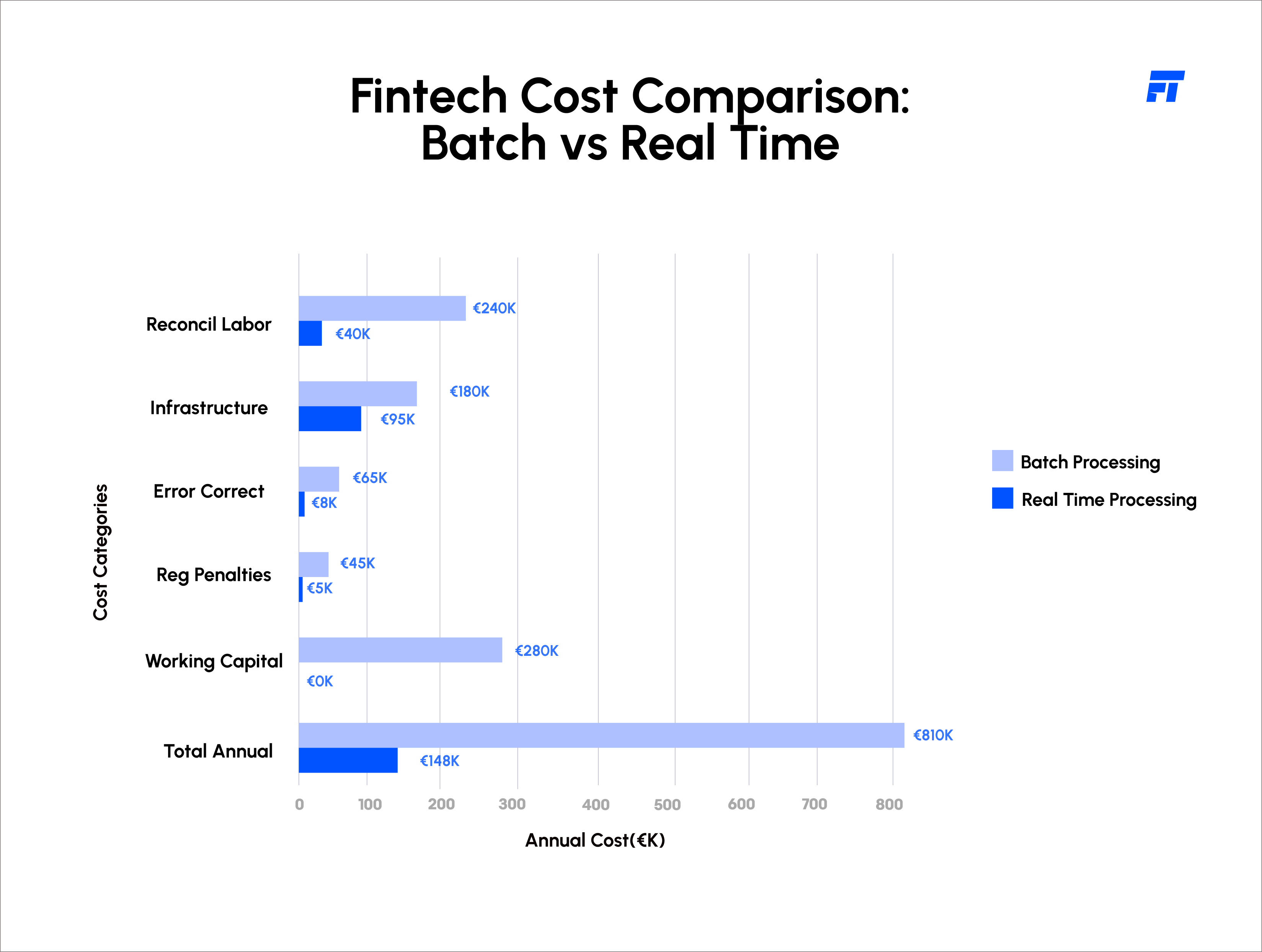

Most large banks still rely on batch processing, where transactions queue throughout the day and settle overnight. This dated approach now costs money, slows innovation, and creates friction that competitors have eliminated.

Real-time ledgers change this. Instead of end-of-day settlement, real-time systems process each transaction immediately, delivering instant confirmations and current account balances. The impact is measurable: institutions migrating to real-time architectures reduce core IT costs by 25 to 50 percent, accelerate product launches from 12 months to 4 months, and improve customer satisfaction. For a mid-sized bank with $20 million in annual core spending, this means $5 to $10 million in freed capital annually.

The question is no longer whether to modernise, but how quickly. Understanding the financial case and technical trade-offs is essential to informed decision-making.

Batch processing once made economic sense. Today, it is unsustainable on three fronts.

Only 5 percent of banks modernise their core annually, yet 70 percent of executives are reviewing core strategy. This gap reflects uncertainty about approach and ROI.

Real-time ledger systems represent a fundamental architectural shift. Rather than batching transactions for periodic processing, these systems process each transaction individually as it occurs updating ledgers and compliance records instantaneously. How It Works:

Real-time systems are built on event-driven architectures. Each transaction triggers a discrete event that flows through the system independently. Multiple transactions process simultaneously without blocking one another. Key architectural components include:

Real-time systems are more resilient. Distributed architectures isolate failures; if one microservice fails, others continue processing. Batch systems have single points of failure; a job failure prevents thousands of transactions settling. Regulators recognise this: FCA and DORA mandate resilience, and distributed architectures meet this naturally.

Compliance becomes automatic. Real-time systems embed regulatory rules into ledger logic with complete auditability. This contrasts batch systems where compliance involves post-hoc analysis and manual reconciliation. Research on blockchain-based real-time ledgers shows 67 to 92 percent reductions in manual intervention and 88 to 97 percent reductions in disputes.

Fraud gets caught instantly. Real-time ledgers enable immediate fraud detection via machine learning. Batch systems process fraudulent transactions normally, making real-time detection impossible. This latency is where most fraud occurs.

Phased migration minimises disruption. Keep legacy systems operational whilst gradually migrating functions and customer cohorts to real-time platforms. Run parallel systems with robust reconciliation during transition. Use phased cutover that allows rapid rollback. Zions Bancorporation successfully executed this over multi-year timelines, retiring legacy systems in 2023 after starting in 2011.

Trust becomes visible. Instant confirmations, current balances, faster dispute resolution build loyalty. Merchants gain better cash flow and working capital management. Speed becomes competitive advantage. Product cycles cut from 12 months to 4 months enable rapid market response. Institutions moving first establish positions followers struggle to recapture.

Compliance strengthens, not constrains. Real-time, API-first architectures satisfy regulatory resilience expectations naturally. Compliance becomes competitive advantage, not cost centre. Cost structure compounds advantages. Modernised institutions have dramatically lower cost-to-serve than batch-based competitors. Freed capital reinvests into customer acquisition, innovation, and expansion. Over five years, this compounds into substantial advantage.

Partnerships become possible through APIs. Real-time ledgers built API-first position institutions for partnerships with fintechs, payment networks, and ecosystem players. This enables embedded finance, white-label, and marketplace participation batch architectures make difficult.

Legacy batch systems are economically, operationally, and strategically unviable. They consume disproportionate IT budgets, constrain innovation, and fail to meet regulatory resilience expectations. By 2028, outdated systems will cost global banks $57 billion annually.

Real-time ledgers deliver proven returns: cost reduction, faster launches, better customer experience, and regulatory resilience. They are proven in production globally.

Progressive modernisation is pragmatic. Dual-core strategies keep legacy systems operational whilst real-time capabilities power new products, new segments, and new payment rails. This spreads cost, reduces risk, and delivers visible benefits within months.

The competitive window is closing. Institutions moving now set standards others follow. Those delaying face accelerating disadvantage.

Your ledger architecture will determine competitive position for the next decade. Decide now.

Ready to explore how Fyscal Technologies can help you achieve this?

.png)

.svg)