Crypto and Stablecoin Cards: Bridging Digital and Fiat

Explore how stablecoin linked cards are transforming digital assets into everyday spending tools, driving institutional growth and retail utility in 2026.

Explore how stablecoin linked cards are transforming digital assets into everyday spending tools, driving institutional growth and retail utility in 2026.

Subscribe now for best practices, research reports, and more.

The global financial system is witnessing a structural shift where the boundary between decentralized finance and traditional retail commerce is effectively dissolving. For the better part of a decade, digital assets were viewed primarily through the lens of speculation or long term stores of value. However, the emergence of high performance blockchain infrastructure has facilitated a new phase of utility. Consumers no longer wish to merely hold assets: they expect the ability to deploy them with the same fluidity as sovereign currency.

This demand has birthed the rapid proliferation of crypto and stablecoin linked cards. These instruments serve as the critical bridge between digital wallets and the existing global network of over 150 million merchant terminals. By the end of 2025, the adoption curve for these products reached a significant inflection point. According to data from Visa, spending across partnered crypto card programs surged by 525 percent over the course of a single year. This growth indicates that digital assets have moved from experimental use cases into the realm of regular financial behaviour.

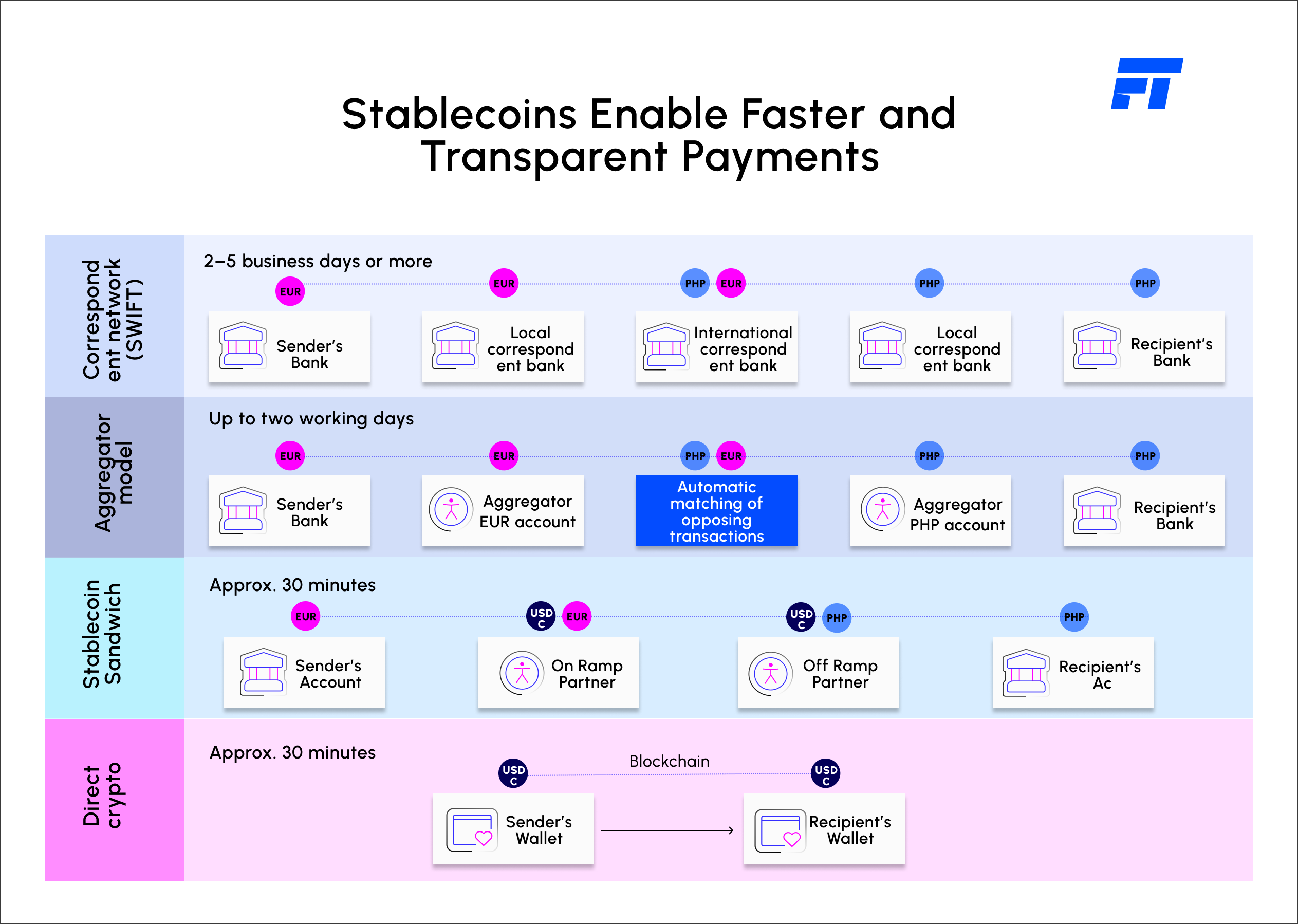

The primary tension in the digital asset ecosystem has historically been the friction associated with "off ramping." For a consumer to spend their holdings at a physical retailer, they traditionally faced a multi step process involving manual exchanges, bank transfers, and multi day settlement delays. This friction acted as a ceiling for the retail utility of blockchain technology.

Modern stablecoin cards resolve this tension by utilizing an architecture that makes the underlying rail invisible to the end user. When a transaction occurs, the conversion from a digital token, such as USDC or EURC, into local fiat currency happens at the exact moment of authorization. The merchant receives settled fiat currency through their standard acquiring partner, while the consumer experiences a familiar "tap to pay" interface.

This model relies on a stabilized technical stack that unifies custodial or self custodial wallets with traditional card networks. In 2025, monthly crypto card volumes reached approximately 1.5 billion dollars, a figure driven by the fact that stablecoins provide the price predictability necessary for day to day commerce. Unlike volatile cryptocurrencies, fiat backed stablecoins allow for accurate retail pricing and recurring payment schedules, making them the preferred "meat" of the payment sandwich.

For senior decision makers at banks and B2B fintech platforms, the shift toward card based digital asset spending represents a significant opportunity to capture new profit pools and defend existing ones. The business impact is quantifiable across three primary dimensions:

The decision path for implementing a stablecoin card program has been significantly cleared by recent regulatory milestones. The passage of the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act and the implementation of Europe’s Markets in Crypto Assets (MiCA) regulation have provided the federal frameworks required for institutional confidence. These laws ensure that compliant stablecoins are backed 1:1 by high quality liquid assets, effectively treating them as regulated financial instruments rather than speculative tokens.

However, the execution risk remains high for institutions attempting to build these systems in house. Integration requires a modular approach to core banking modernisation, ensuring that legacy ledgers can communicate with on chain protocols through secure API first architectures. Decision makers must weigh the trade offs between fully managed "card as a service" models and self managed infrastructures that offer greater control but higher operational overhead.

Successful digital transformation in this space requires more than just a new product launch: it requires a fundamental re engineering of the money stack. Fyscal Technologies (FT) serves as a vendor agnostic partner for institutions navigating this transition. We help banks and fintechs build the resilient, API first architectures necessary to support stablecoin cards without becoming trapped in proprietary vendor ecosystems.

Our consulting approach focuses on "compliance by design," ensuring that KYC, AML, and real time transaction monitoring are embedded directly into the payment flow. By decoupling the card surface from the underlying pot of funds, we enable institutions to offer their customers the flexibility to spend from multiple asset classes while maintaining a single, unified user experience.

The organisations that move first to adopt these wallet native spending tools will not only capture a larger share of the global payments market but will also position themselves as the primary financial interface for the digital native economy. The strategic question for 2026 is no longer whether to integrate digital assets, but how to do so with the agility and resilience required to stay competitive.

Ready to explore how Fyscal Technologies can help you achieve this.

.png)

.svg)