Request-to-Pay (R2P): The Feature That Kills the Direct Debit

Request-to-Pay (R2P): The Feature That Kills the Direct Debit

R2P replaces direct debit with real-time two-way payments. Instant execution, higher approval rates, customer control. 4.7% revenue uplift.

Written By

FT Scholar Desk

SHARE THIS

Unlock exclusive FyscalTech Content & Insights

Subscribe now for best practices, research reports, and more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Heading 1

Heading 2

Heading 3

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Direct debit–style push payments are structurally misaligned with real-time finance. The future of recurring collections is customer-approved, two-way Request-to-Pay.

Direct debit is a biller push with late consumer visibility and week-long recovery from failures.

Payments are treated as one-way instructions, not interactive decisions.

R2P delivers instant digital requests inside the banking app.

Customers can approve, decline, or reschedule before settlement.

Approval triggers immediate final payment on real-time rails.

Networks are steering adoption toward 2030, making delays costly

Early R2P transition gives institutions control and revenue certainty; waiting forces expensive retrofits and leaves legacy push payments behind modern risk.

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Type image caption here (optional)

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Direct debit’s push model creates delayed visibility, persistent risk exposure, and costly recovery cycles making recurring payments misfit for real-time digital banking.

One-way, asynchronous flow – Biller initiates; customers see details days later outside the banking app; processing is retrospective.

Late failure discovery – 3–5 business days to know a debit failed; recovery then stretches for weeks.

Involuntary churn – Consumers with expired cards lose subscriptions without warning; billers can’t confirm request receipt.

Static mandates = open door – Single authorisation persists indefinitely; issuers can’t separate stolen-credential debits from real ones.

High false positives – Broad declines hit legitimate users even with funds.

Onboarding friction – Requiring card entry, mandate setup, and waiting drives abandonment and rising acquisition cost.

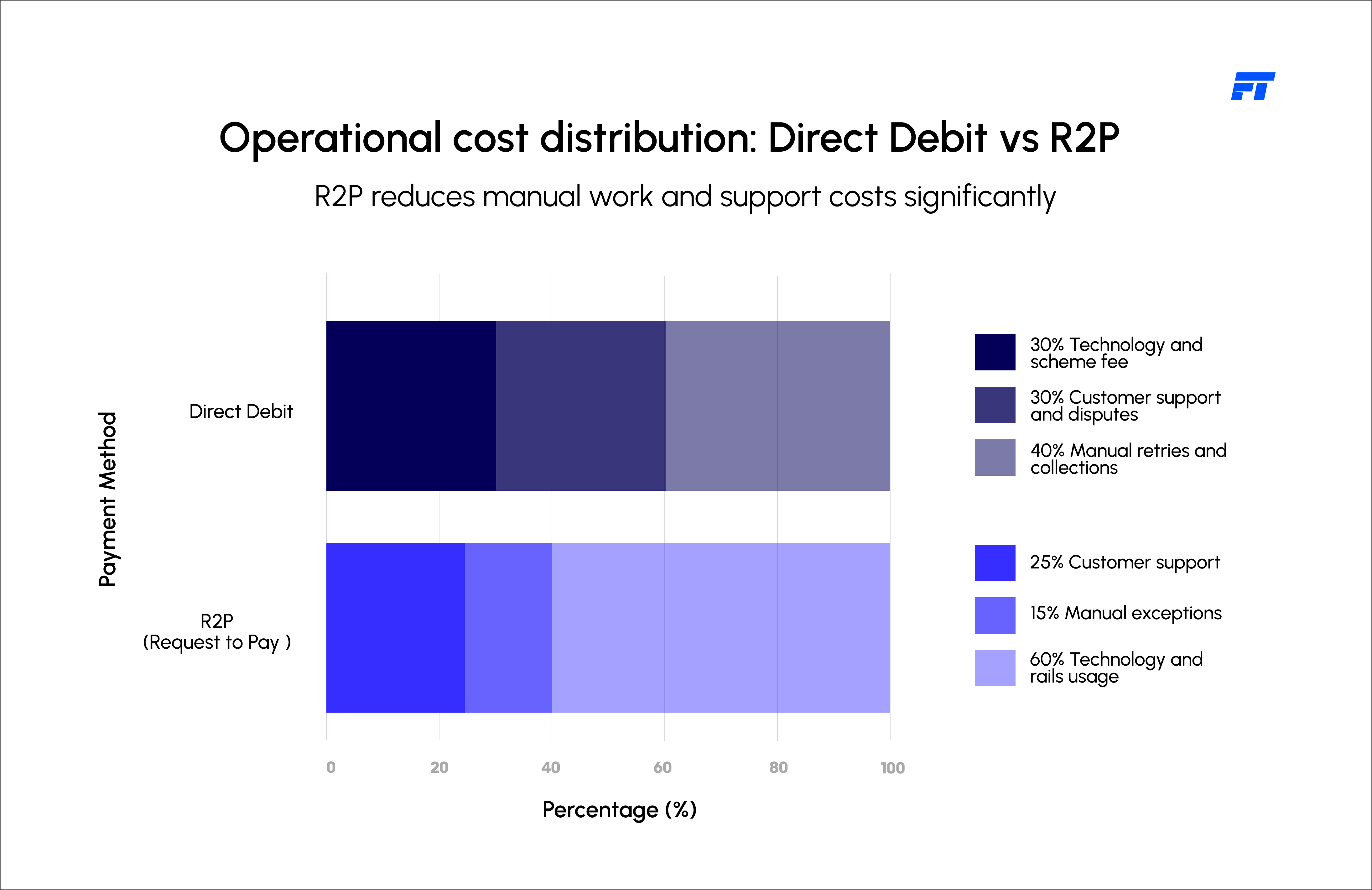

Cascade from 8–10% failures – Retry logic, manual follow-ups, investigations, and cross-team processes create hidden costs.

Sector impact – For utilities, telco, insurance: 5–10% revenue risk annually; for merchants/marketplaces: support burden and churn that outweigh fees.

Takeaway Push-initiated direct debit is structurally broken for modern finance. Recurring collections must move to continuous, customer-approved, real-time Request-to-Pay to reduce fraud, protect consumers, and cut operations by nearly half.

R2P as Payment Architecture Shift

Request-to-Pay is not a feature upgrade it is a payment-architecture shift that moves recurring collections from biller push to customer-controlled pull on real-time rails.

Clear definition – Payee sends a structured Request for Payment; payer approves, schedules, splits, or selects account inside their banking app before funds move.

Industry inversion – Customers shift from passive post-fact notifications to explicit pre-settlement decisions.

Operational impact – Visibility becomes real time; mandate risk and retry cycles largely disappear.

Bank strategy – R2P is emerging as the future core infrastructure versus legacy direct debit.

Processor/fintech advantage – Native R2P platforms attract merchants and create stronger user experience and lock-in.

Market signal – UK banks and global networks increasingly rate R2P superior to traditional push models.

Takeaway Institutions that adopt R2P early gain control, trust, and collection certainty; those that remain on direct-debit push will face isolation and costly retrofits as merchants migrate to two-way real-time payment ecosystems.

Real-Time Execution

Merchants relying on direct debit manage cash flow around a 3–5 day clearing cycle, which traps funds in float and delays seller payouts and subscription reconciliation.

Legacy timeline burden: Direct debit clears in 3–5 days, creating a week of uncertainty for merchants and seller payouts.

Instant inversion: R2P collects only after customer approval and settles in seconds with automatic reconciliation.

Category impact:

B2B invoices paid same/next day → DSO drops from ~30–45 days to near-instant.

Utilities and marketplaces release millions in trapped working capital.

Subscriptions recover failures within hours, cutting involuntary churn.

Takeaway: Cash flow shifts from delayed float to instant predictability.

Customer Control & Trust

Direct debit fails 8–10% on first attempt due to expired cards, mandate revocation, and broad fraud declines, forcing multiple retries over weeks.

Direct debit weakness: 8–10% first-attempt failures from expired cards, mandate revocation, and broad fraud declines.

R2P dynamic: Payer sees full details in banking app and approves upfront; funds visibility confirmed before execution.

Results:

95% first-time success versus ~90% for legacy.

20–30% churn reduction in subscription businesses.

Lower fraud as context flows through the customer’s bank, not biller claims.

Takeaway: Control lifts success by ~5% and recovers revenue lost to retries and bounce.

Cross-Border Reach

Direct debit fails 8–10% on first attempt due to expired cards, mandate revocation, and broad fraud declines, forcing multiple retries over weeks.

Domestic limitation: Direct debit schemes are market-specific and expensive to replicate.

Interoperable rails: R2P rides on SEPA Instant, Faster Payments, UPI, PayNow, PromptPay using standard messaging.

Expansion wins:

Implement once → extend across countries without rebuild.

Takeaway: Growth moves from local fragmentation to global standardisation.

Strategic Impact for the C-Suite

R2P turns recurring payments into transparent, customer-approved real-time infrastructure—closing fraud gaps that legacy direct debit creates.

Strategic Impact

Trust: customers see and verify requests before settlement, reducing surprise charges and involuntary churn.

Competitiveness: early adopters position as innovation leaders; superior UX attracts merchants from push-only processors.

Resilience: >95% success collapses retries and exceptions; architecture simplifies around approval workflows.

Innovation: instalments, BNPL, and on-demand payouts integrate natively without technical debt.

Efficiency: less manual review → millions saved for large institutions and >20% cost drop for smaller merchants.

Compliance: regulatory timelines align with R2P rails; controls like data minimisation and fraud prevention are built-in traits.

Takeaway Shift to R2P now for higher acceptance, lower fraud, leaner operations, and regulatory certainty—or face expensive retrofits and legacy isolation by 2030.

Conclusion and Forward-Looking Perspective

Direct debit remains the backbone of recurring payments, but its biller-push, delayed-notification design is misaligned with real-time digital banking. Merchants and marketplaces manage around 3–5 day clearing cycles, creating uncertainty in cash flow and operational friction for users who only see outcomes after execution.

Request-to-Pay flips this model by placing structured requests inside the customer’s banking app before funds move. Payers can approve, decline, or reschedule in seconds, with settlement occurring immediately upon consent. This two-way flow improves visibility, accelerates B2B receipts, and sharply reduces retries and exception handling.

For leadership, R2P is a strategic infrastructure shift that unlocks higher acceptance, lower fraud exposure, and nearly half the operational cost. Early movers capture advantage, while delays invite expensive retrofits. The prudent step is to begin a planned R2P transition with Fyscal Technologies now.

.png)

.svg)