AI and Fraud in Fintech: Why Deepfakes and Synthetic IDs Are Winning

Deepfake fraud up 200%+ globally. Phishing, identity theft, money muling exploding. Legacy fraud controls are failing. Here's what adaptive defences look like.

Deepfake fraud up 200%+ globally. Phishing, identity theft, money muling exploding. Legacy fraud controls are failing. Here's what adaptive defences look like.

Subscribe now for best practices, research reports, and more.

The Data Contradiction

What This Really Means

Imagine you're a bank CEO reviewing fraud metrics. Last year: 1.5% fraud rate. This year: 1.3% fraud rate. You relax. Fraud is down 14.6%. But underneath that headline, something darker is happening: deepfakes went from 100 attacks to 337. You just don't see it in the aggregate numbers.

You're measuring "fraud incidents caught" but not "AI-powered identity attacks attempted." It's like celebrating lower car theft while missing a spike in sophisticated key-cloning attacks.

The data tells two stories:

Deepfakes are reshaping digital banking fraud. The problem isn’t anomalies anymore it’s authenticity, and traditional controls were never designed for that shift.

Why traditional systems miss deepfakes

Takeaway — The risk you don’t see

Consumers face phishing-driven account takeover, while businesses are hit through direct identity and admin-credential compromise with faster, larger losses.

Key breakdown

Takeaway: Fraud strategy must match user type phishing resilience for consumers, authenticity and governance for businesses; otherwise prevention will lag behind payouts.

Across regions, users clearly recognize that fraud is turning AI-driven, yet most institutions still operate on legacy protections. This gap between belief and execution is becoming a core risk for digital finance.

Breakdown

Takeaway: Consumer awareness is running ahead of institutional readiness. Fraud strategy must shift to continuous, real-time authenticity detection and admin-activity monitoring otherwise prevention will remain behind AI-powered transfers despite healthy-looking dashboards.

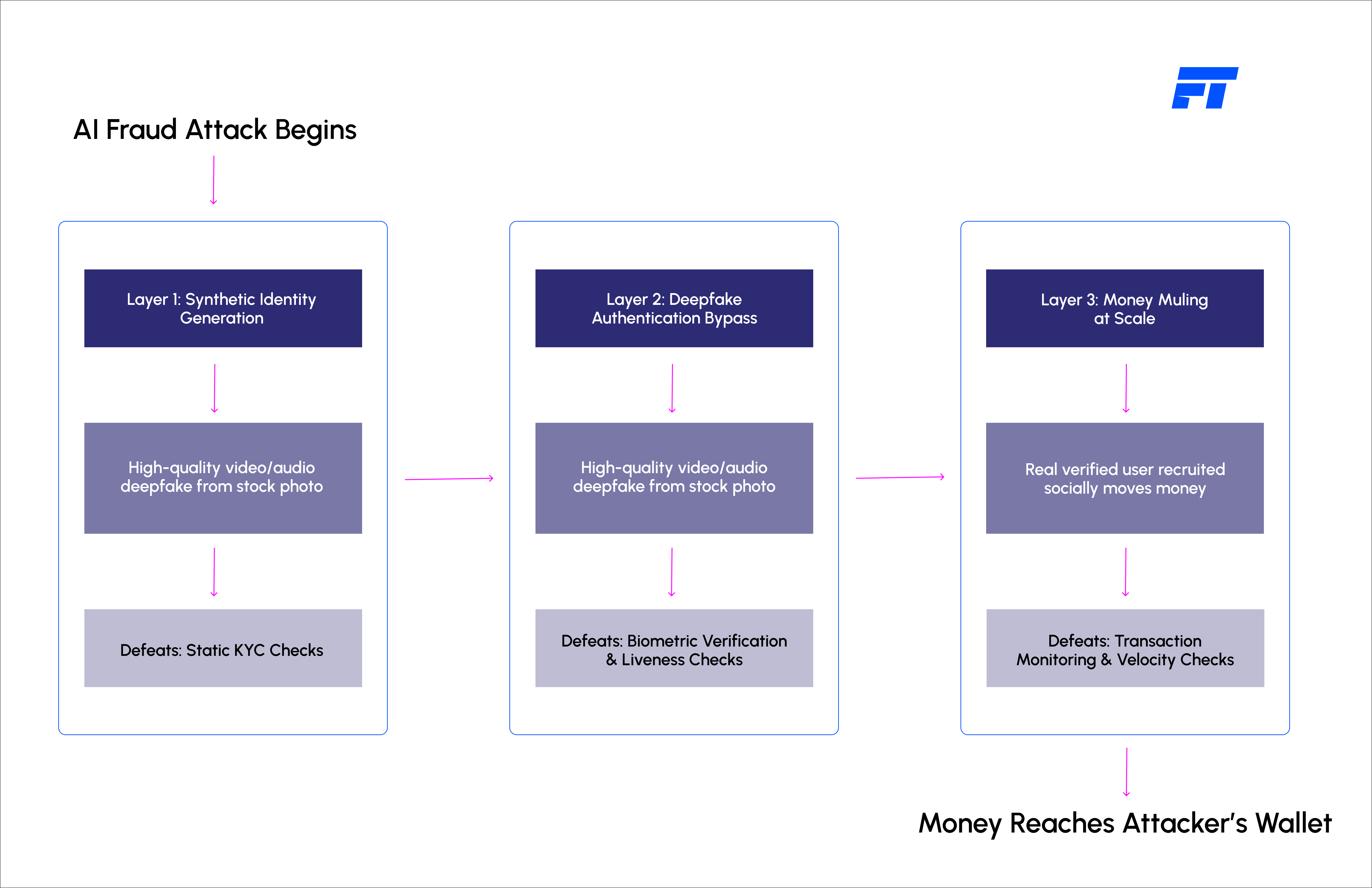

Money muling has shifted from a niche crime to a scalable, social-media–driven laundering industry. Verified customers and fast payout rails are now being used as infrastructure for organised mule rings.

Breakdown — The reality of muling

Verified users can become laundering nodes without institutions seeing the graph. Fraud control must move to network-level, real-time flow monitoring and payout governance or modern rails will continue converting your platform into a high-velocity mule engine.

Instead of static rules and batch checks, build continuous, AI-native fraud systems

Real-Time Behaviour Scoring:

Deepfake-Aware Biometrics:

Network & Graph Analysis:

Dynamic Step-Ups:

Integration as First-Class Product Feature:

Takeaway: Fraud is no longer compliance. It's a trust layer. It lives in every user journey, not just in a separate risk team

Strong support for tighter rules exists everywhere . But regulation is slow, attackers are fast [file:88]:

What Regulation Can Do:

What Regulation Cannot Do:

Takeaway: Regulation creates a floor; your own adaptive systems create a ceiling attackers cannot break through [file:88].

The data is clear: AI-powered fraud is not a future risk; it is embedded in your funnel today

The companies winning are those treating fraud as a core product responsibility, not a compliance checkbox. They are shipping continuous detection, dynamic policy engines, and network analysis as standard infrastructure

The companies losing are those still running batch processes, static rules, and manual reviews designed for a pre-AI world.

The fraud game has changed. Your defences need to change with it, or you will find out too late.

Ready to move from static rules to adaptive, AI-native fraud detection?

Talk to Fyscal Technologies about continuous identity and fraud infrastructure.

.png)

.svg)