Why Tokenization Is Finally Becoming Real: Strategies for Financial Institutions

$30B RWA market, 308% growth in 3 years, $30T potential by 2034. Why tokenization is now strategic priority for financial institutions.

$30B RWA market, 308% growth in 3 years, $30T potential by 2034. Why tokenization is now strategic priority for financial institutions.

Subscribe now for best practices, research reports, and more.

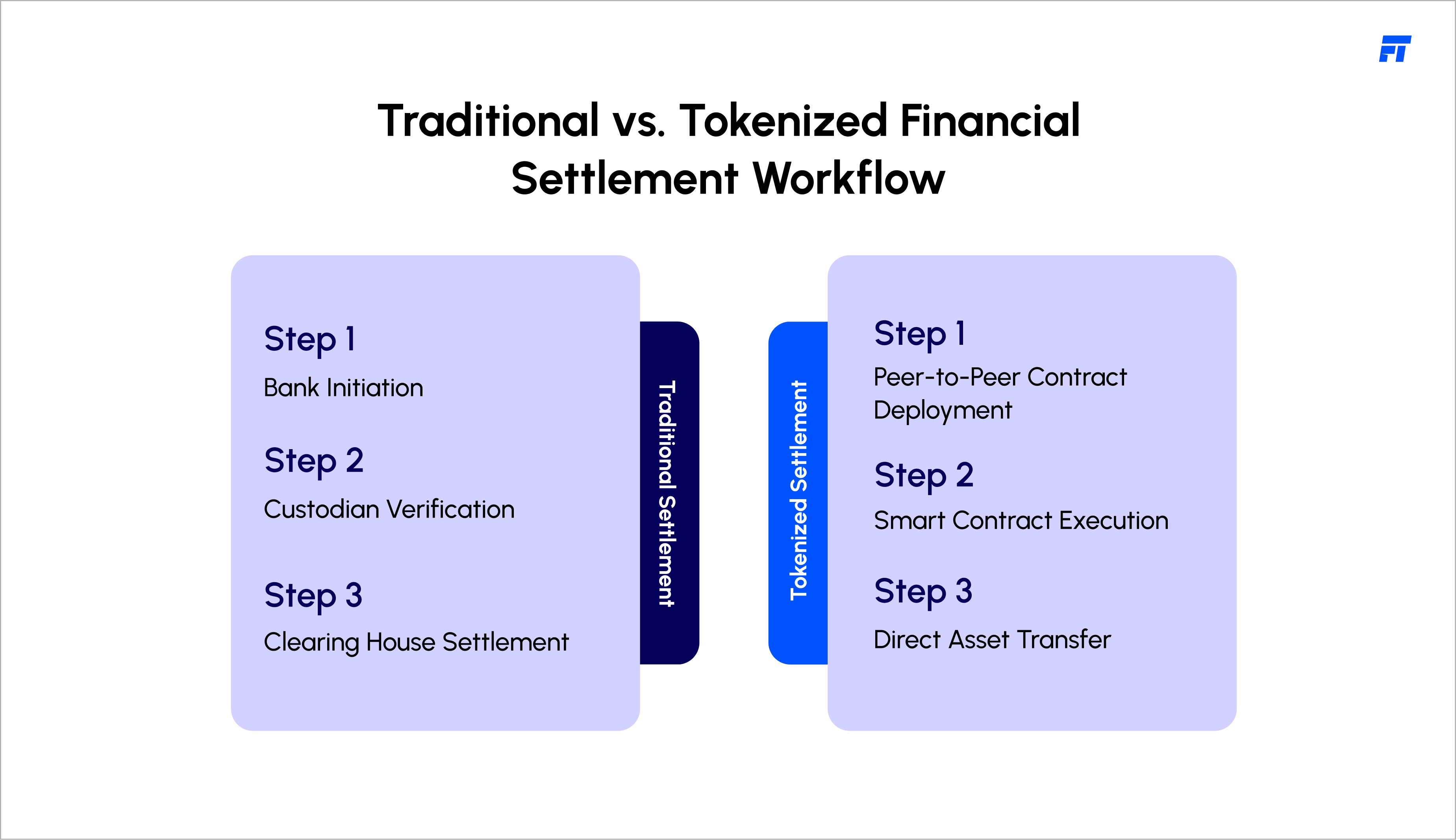

Tokenization has transitioned from speculative concept to operational reality. This is not a "watch this space" moment. This is an immediate strategic imperative.

The evidence is unmistakable. The RWA (real-world assets) tokenization market reached $30 billion in Q3 2025, representing a 10x increase from 2022 levels of $2.9 billion. The market grew 308 percent over three years and is projected to reach $30 trillion by 2034. On 11 November 2025, IOSCO published its Final Report on Tokenisation of Financial Assets, establishing regulatory frameworks and acknowledging tokenization as a permanent feature of financial markets.

What distinguishes this moment from previous hype cycles is institutional adoption. BlackRock's Larry Fink declared in January 2024 that tokenization of every stock and bond on a general ledger is inevitable. This is not innovation rhetoric. This is institutional commitment.

What financial institutions gain by acting now:

Legacy financial infrastructure was built for a world of limited participants, manual processes, and accepted delays. That world cannot support the transaction volumes, transparency, and speed that emerging markets and institutional demand require.

The structural challenge remains the lack of interoperability across blockchains and lack of high-quality settlement assets. Institutions that solve these challenges first will capture disproportionate opportunity.

Tokenization is finally becoming real because three prerequisites are now satisfied simultaneously.

These three factors converging create a market tipping point. Institutions delaying now are delaying against regulatory tailwind, proven infrastructure, and institutional demand.

Imperative 1: Reposition from Speculation to Core Infrastructure

For years, financial institutions discussed tokenization as potential future innovation. That narrative is obsolete. Tokenization is core infrastructure transformation competing with legacy systems for asset flows.

Asset classes converting to tokenization fastest include:

Institutions should assess which products in their portfolio would most benefit from tokenization, questioning whether tokenization can accelerate strategic priorities such as entering new markets or attracting new customer segments.

This is not product innovation. This is asset class reallocation.

Imperative 2: Build Vendor-Agnostic, Interoperable Infrastructure

The structural challenge identified by regulators is lack of interoperability across blockchains. Institutions building monolithic tokenization solutions dependent on single blockchain networks will discover their infrastructure becomes stranded as market consolidates around interoperable standards.

Strategic imperative is building infrastructure that:

Financial institutions engaging with new financial market infrastructure create possibilities along the value chain for cost savings, net new revenues, or opportunities to reduce risk. This requires vendor-agnostic execution preventing lock-in.

Imperative 3: Capture Emerging Market and Emerging Asset Class Opportunity

Real estate tokenization is projected to reach $4 trillion by 2035 (compared to under $0.3 trillion in 2024). This represents capital that will flow to institutions offering tokenized solutions. Tokenization democratises investment by enabling fractional ownership, allowing middle-class investors access to premium properties with lower entry costs.

Similar opportunities exist across:

Institutions building native tokenization infrastructure now establish competitive advantage in capturing this emerging opportunity.

Tokenisation is not a future scenario. It is a present reality. Luxembourg and Singapore are positioning as global tokenization hubs through comprehensive regulatory frameworks. Dp BlackRock, Vanguard, and State Street are all actively building tokenisation capabilities and exploring asset issuance.

The question financial leadership faces is not whether tokenization will reshape asset markets. The question is whether your institution will lead that reshaping or play catch-up to competitors that moved faster.

Tokenisation has transitioned from emerging technology to strategic imperative. Regulatory frameworks are established. Infrastructure is proven. Institutional demand is undeniable. Market projections show $30 trillion opportunity by 2034.

Institutions acting now establish competitive advantage through network effects, customer access, and operational efficiency that competitors cannot easily overcome. Institutions delaying will find themselves competing in markets already established by early movers.

The strategic imperative is clear: assess your asset classes, identify tokenization opportunities that accelerate strategic priorities, build vendor-agnostic infrastructure that avoids lock-in, and capture emerging market and asset class opportunity before competitors do. Tokenisation is finally becoming real. The question is whether your institution will lead.

Ready to explore how Fyscal Technologies can help you achieve this?

.png)

.svg)