How Banks Can Modernise Merchant Services & Compete With Stripe, Adyen, and Shopify

40% of merchants plan to move to PayTechs. Here’s why banks are losing ground and the four strategic shifts needed to rebuild modern, cloud-native merchant services.

40% of merchants plan to move to PayTechs. Here’s why banks are losing ground and the four strategic shifts needed to rebuild modern, cloud-native merchant services.

Subscribe now for best practices, research reports, and more.

Banks didn’t lose merchant services in a single moment. They lost them click by click, while PayTechs quietly built what merchants actually needed: speed, simplicity, reliability, and growth tools.

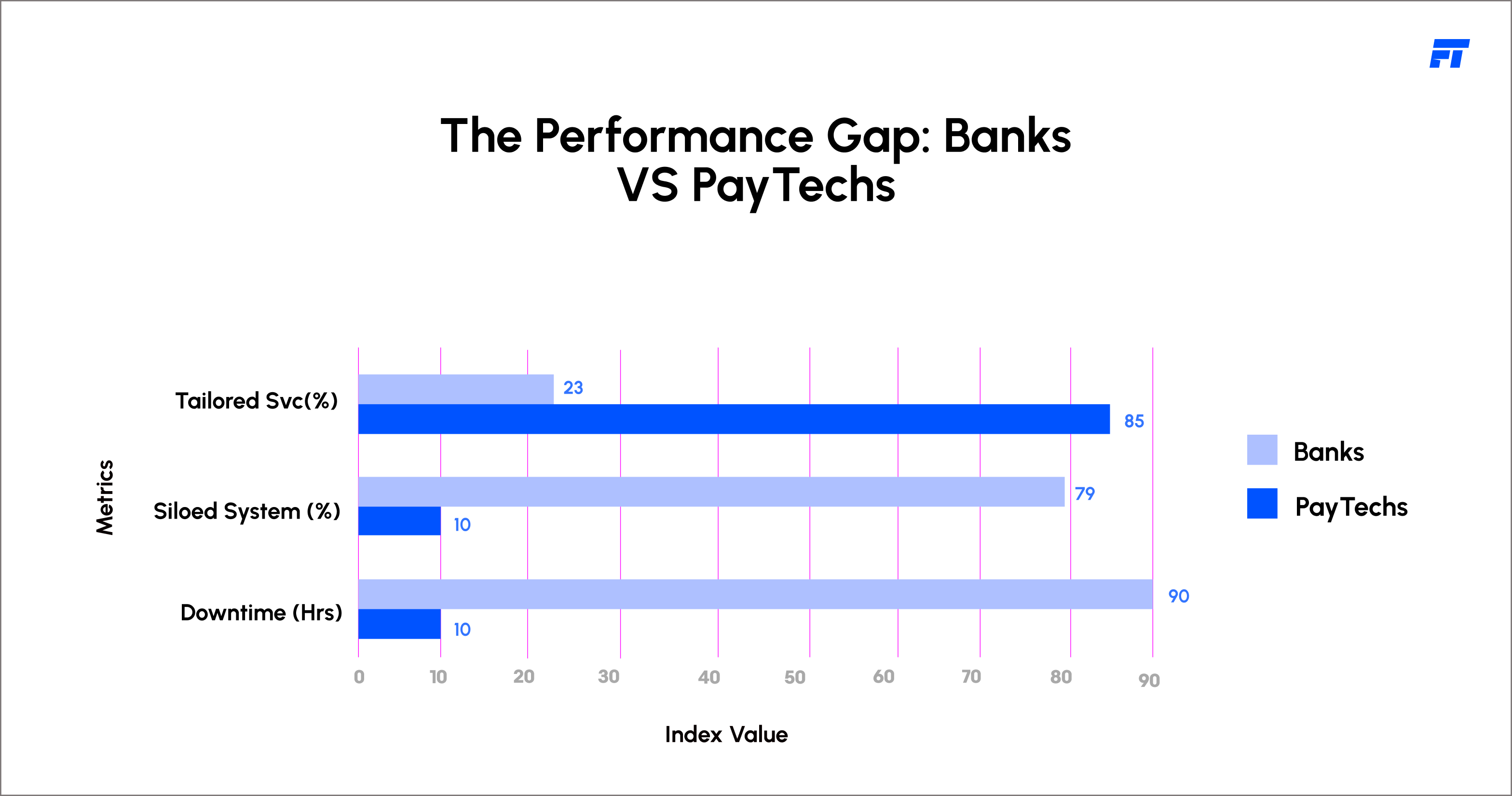

Across the past decade, as banks strengthened compliance, managed regulatory load, and expanded issuing products, players like Stripe, Adyen, and Shopify redefined what “serving merchants” means. The contrast is now undeniable. According to Capgemini’s World Payments Report 2026, nearly 40% of small and mid-sized merchants plan to switch from banks to PayTechs within the next 12 months.

This isn't a niche trend, it’s a structural shift. Banks that misread the reasons behind this movement will continue managing legacy relationships while competitors build the future of merchant ecosystems.

The drivers behind merchant migration are clear, measurable, and accelerating:

Despite the shift, banks aren’t out of the race. They still possess structural strengths PayTechs cannot easily replicate:

The question isn’t can banks win back merchants? It’s whether they will act fast enough.

Banks that embrace these moves will not just compete with PayTechs, they will redefine the merchant banking experience.

Imagine a bank where:

This isn’t speculation. Stripe, Adyen, and Shopify already built this. Banks can build it too, but not if they wait.

Banks have a right to win merchant services, but not by playing yesterday’s game. To close the widening gap, they must shift from legacy processors to platforms: connected, intelligent, cloud-native, and fast. Merchants have already made their expectations clear. PayTechs answered with speed. Banks must answer with transformation.

The window to act is narrowing, but it’s still open. Ready to explore how Fyscal Technologies can modernise your merchant services infrastructure and help you compete with PayTechs?

Book a Strategy Consultation →

.png)

.svg)