Visa’s Stablecoins Advisory Practice: Why Stablecoins Are Moving From Experiment to Payment Infrastructure

Visa’s Stablecoins Advisory Practice: Why Stablecoins Are Moving From Experiment to Payment Infrastructure

When Visa launched a dedicated Stablecoins Advisory Practice across Europe, it was not announcing a new product. It was signalling a shift.

Written By

FT Scholar Desk

SHARE THIS

Unlock exclusive FyscalTech Content & Insights

Subscribe now for best practices, research reports, and more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Heading 1

Heading 2

Heading 3

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

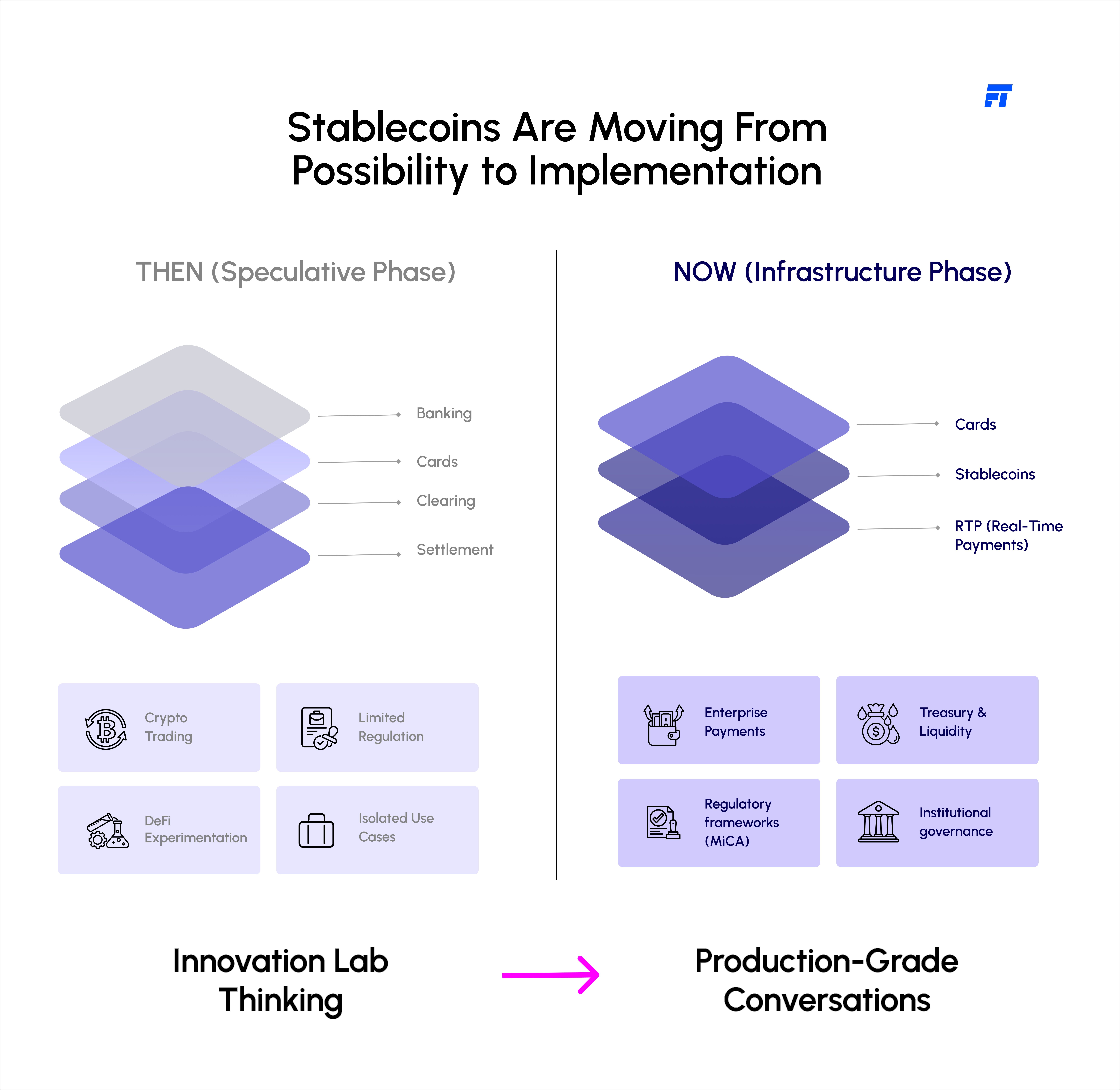

Visa does not build advisory practices around speculative trends. It does so when a technology is moving from possibility to implementation. In this case, stablecoins are no longer being treated as fringe crypto instruments they are being positioned as emerging payment infrastructure that banks, merchants, and enterprises need to understand, govern, and integrate responsibly.

This move reflects a broader transition underway in global payments: stablecoins are leaving the innovation lab and entering regulated, enterprise-grade conversations.

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Type image caption here (optional)

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

For much of their existence, stablecoins were discussed primarily in the context of crypto trading and decentralised finance. That framing is changing.

Today, stablecoins are increasingly evaluated through a payments lens:

Faster settlement

Lower cross-border costs

Programmable money

Always-on availability

At the same time, regulators particularly in Europe are defining clearer frameworks around issuance, custody, and usage. With MiCA (Markets in Crypto-Assets Regulation) taking shape, the conditions for institutional participation are solidifying.

According to McKinsey, stablecoins have the potential to materially improve cross-border payments and treasury operations when deployed within compliant, well-governed frameworks. Visa’s advisory move aligns with this assessment.

Why Visa Is Stepping In Now

Visa sits at the centre of the global payments ecosystem. Its role is not just to process transactions, but to maintain trust, interoperability, and scale across participants.

By launching a Stablecoins Advisory Practice, Visa is responding to growing demand from:

Banks exploring stablecoin settlement and tokenised deposits

Enterprises evaluating treasury and liquidity use cases

This is not about replacing existing card rails. It is about helping institutions understand where stablecoins fit alongside them and where they don’t.

BCG notes that the next wave of payments innovation will be driven less by new rails alone and more by orchestration across traditional and digital infrastructures. Advisory becomes critical in this transition.

Stablecoins as a Payments Infrastructure Layer

What makes stablecoins structurally different from earlier payment innovations is their dual nature. They are both:

A store of value, pegged to fiat currencies

A transfer mechanism, operating on programmable networks

This combination enables use cases that are difficult to achieve with legacy systems:

Near-instant cross-border settlement

24/7 payments without batch cutoffs

Atomic settlement linked to business logic

Reduced reliance on correspondent banking chains

However, these benefits only materialise when stablecoins are integrated into existing payment, compliance, and treasury systems not when they operate in isolation.

Visa’s advisory focus highlights a key reality: stablecoins do not eliminate complexity; they relocate it.

The Questions Banks and Enterprises Are Asking

As stablecoin adoption moves closer to production environments, institutions are grappling with practical questions:

How do stablecoins coexist with existing card, ACH, and RTP rails?

Where does custody sit on a balance sheet or via partners?

How are AML, sanctions screening, and transaction monitoring enforced?

What happens during volatility, de-pegging events, or network outages?

How do accounting, reconciliation, and reporting adapt?

McKinsey highlights that governance, risk, and operational readiness not technology are now the primary blockers to institutional stablecoin adoption. Visa’s advisory practice exists precisely to help organisations answer these questions before deploying at scale.

Europe as the Proving Ground

Europe is a logical starting point for this initiative.

With MiCA providing regulatory clarity and strong payment infrastructure already in place, Europe offers a controlled environment to explore stablecoin-based use cases without regulatory ambiguity.

This does not mean mass adoption is imminent. It means structured experimentation is becoming acceptable and in some cases, necessary for institutions that want to remain competitive in cross-border payments and treasury services.

What This Means for the Payments Ecosystem

Visa’s move raises the bar for the entire ecosystem.

Stablecoins are no longer just a fintech concern. They are now part of mainstream payments strategy discussions. This has several implications:

Payment providers must prepare for hybrid rails (traditional + tokenised)

Banks need architectures that support programmability and interoperability

Compliance and risk teams must adapt controls to new transaction models

Enterprises will expect faster, more transparent settlement options

In short, stablecoins are becoming a design consideration, even for institutions that choose not to adopt them immediately.

How FT Interprets Visa’s Stablecoin Strategy

At FT, we see Visa’s advisory practice as confirmation that stablecoins are entering the infrastructure decision phase.

The winners will not be those who adopt stablecoins fastest, but those who integrate them most thoughtfully within composable architectures that can support multiple rails, evolving regulation, and changing business needs.

Stablecoins should not sit outside the core payments stack. They should be designed as another rail governed, observable, and interchangeable.

This is where many institutions will struggle, not because of blockchain technology, but because of legacy architecture constraints.

Preparing for a Multi-Rail Payments Future

As stablecoins mature, organisations need to ask a foundational question: Is our payments infrastructure flexible enough to support new rails without destabilising existing ones?

Preparing for this future requires:

Vendor-agnostic orchestration layers

Strong authorisation and compliance controls

Real-time monitoring and auditability

Clear separation between business logic and settlement rails

At FT, we help banks, fintechs, and enterprises design payments architectures that can evolve as stablecoins, real-time payments, and traditional networks converge.

Book a strategy call to explore how your organisation can prepare for a hybrid, multi-rail payments future.

.png)

.svg)