AI-Driven Fraud Detection: Balancing Speed and False Positives in Real-Time Payments

AI-Driven Fraud Detection: Balancing Speed and False Positives in Real-Time Payments

AI-driven fraud detection for real-time payments: learn how to balance accuracy, speed, and customer experience while meeting regulatory requirements and minimizing fraud losses.

Written By

FT Scholar Desk

SHARE THIS

Unlock exclusive FyscalTech Content & Insights

Subscribe now for best practices, research reports, and more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Heading 1

Heading 2

Heading 3

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Real-time payment systems operate at the speed of trust.

A single transaction happens in milliseconds, and your fraud detection system has even less time to decide: approve or block. Get it right, and customers move money instantly. Get it wrong, and you're either exposing your institution to fraud losses or frustrating legitimate customers with false declines both costly outcomes.

This is where AI-driven fraud detection becomes indispensable. But here's what most implementations miss: raw speed isn't enough. The real challenge is balancing detection accuracy with user experience, all while regulatory requirements tighten around you. According to guidance from the Financial Conduct Authority (FCA), financial institutions must implement robust fraud prevention measures that don't compromise customer experience.

Let's walk through how to build a fraud detection system that catches threats without annoying your customers.

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Type image caption here (optional)

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

The stakes are higher than most institutions realize. False positives declining legitimate transactions cost money. Every false decline damages customer trust and drives transaction abandonment. Industry research shows that 34% of customers abandon transactions after a single failed attempt. Multiply that across a large customer base, and you're looking at significant revenue loss.

False negatives missing actual fraud carry their own cost: direct fraud losses, regulatory fines, and reputational damage. Under PSD2 (Payment Services Directive 2), financial institutions are required to implement strong customer authentication and fraud prevention measures, with penalties for compliance failures.

Traditional rule-based systems struggle here. They're built on hardcoded thresholds ("flag if amount > $5,000") that are rigid, slow to adapt, and frequently trigger false alarms. As fraudsters evolve, rule-based systems lag behind.

AI-driven systems learn from patterns in real transaction data, adapting faster than traditional rules. But implementing them poorly without proper calibration can make both problems worse.

Why Traditional Fraud Detection Falls Short in Real-Time Payments

Legacy fraud detection was built for batch processing. A transaction would be flagged, reviewed hours later, and either approved or rejected. That model works when payment settlement takes days.

Real-time payments change everything. You have milliseconds to decide. Here's what breaks down:

Latency constraints: Real-time payments demand sub-second response times. Many traditional systems can't process complex rule sets fast enough without adding noticeable delays.

Adaptive fraud patterns: Fraudsters respond quickly to detection methods. A rule that catches 95% of fraud today might catch only 60% next week as criminals adapt. Static rules become obsolete rapidly.

Data volume: Real-time payment networks generate enormous amounts of transaction data. Traditional systems struggle to process and learn from this volume at scale.

Customer experience pressure: In real-time systems, you can't afford to err on the side of caution. Over-blocking legitimate transactions damages your competitive position.

AI-driven systems address these constraints, but only if you implement them thoughtfully.

Building an AI Fraud Detection System That Works

Start with the Right Data Foundation

AI models are only as good as the data they learn from. Before building anything, ensure you have:

Historical transaction data with fraud labels. You need thousands (ideally millions) of labeled examples transactions marked as legitimate or fraudulent. Without this, your model won't learn effectively.

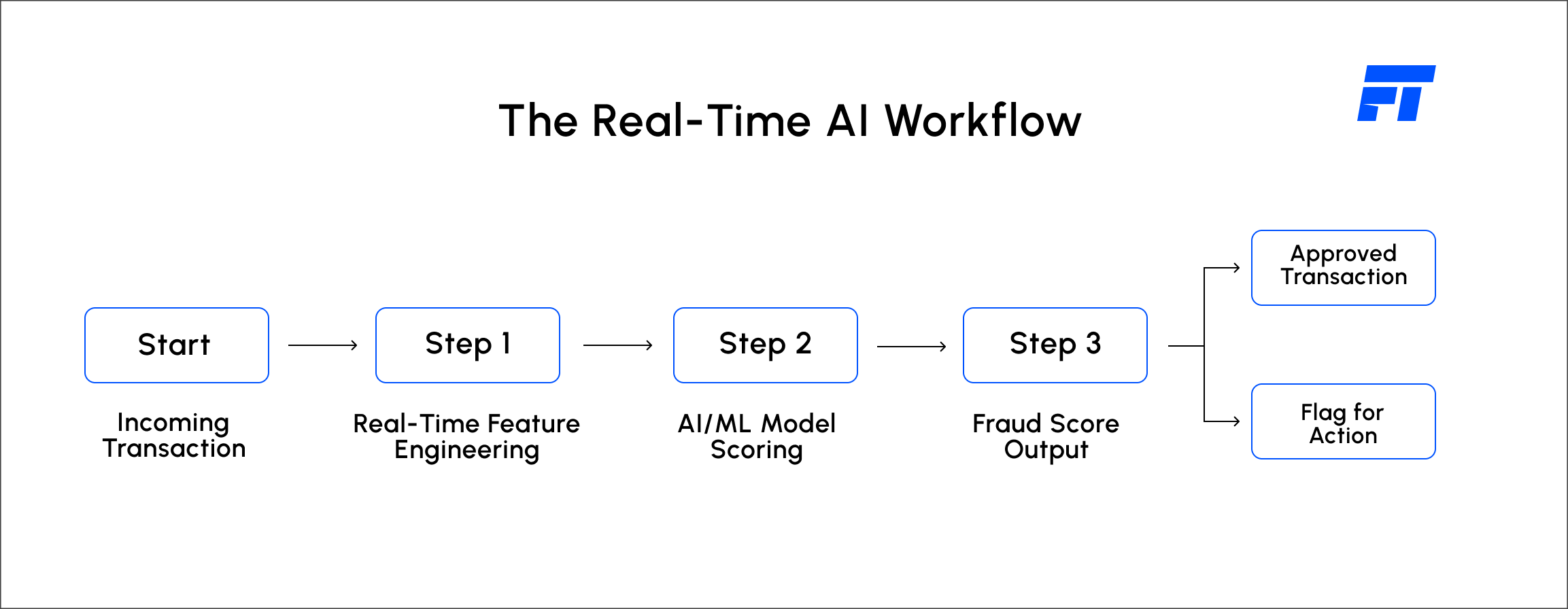

Real-time feature engineering. Build a pipeline that extracts relevant features in milliseconds: customer location, transaction velocity, device fingerprints, peer group behavior, and more. The better your features, the better your model.

Data quality processes. Garbage in, garbage out. Implement validation to catch missing values, outliers, and labeling errors early. For guidance on secure data handling, refer to ISO/IEC 27035 (Information Security Incident Management).

Choose Your Model Architecture Carefully

You have options here, and the best choice depends on your specific constraints:

Gradient boosted trees (XGBoost, LightGBM) are fast, interpretable, and perform well on tabular transaction data. They're a solid default for most real-time payment systems.

Neural networks offer better accuracy on complex patterns but add computational overhead. Reserve these for scenarios where accuracy gains justify the latency cost.

Ensemble approaches combine multiple models, trading some latency for improved robustness. Many production systems use this approach.

The key: test each approach against your specific constraints (latency, accuracy, interpretability) and choose what fits your architecture.

Calibrate for Your Risk Appetite

This is where most implementations fail. Once your model is trained, you need to decide: at what confidence threshold do you approve a transaction?

Set the threshold too high, and you'll catch most fraud but decline legitimate transactions. Set it too low, and you'll miss fraud.

The solution: decision thresholds aligned to business metrics, not just accuracy.

Model the cost of each outcome:

Cost of false positive: lost customer lifetime value from a declined legitimate transaction

Cost of false negative: fraud loss + regulatory cost

Find the threshold that minimizes total cost, not just maximizes accuracy. For most institutions, this means accepting some fraud in exchange for customer experience.

Real-Time Fraud Detection at Scale

When you move from pilot to production, new challenges emerge:

Model drift: Your model learned from historical data, but fraud patterns evolve. Monitor model performance in production and retrain regularly (weekly or daily depending on fraud velocity in your ecosystem).

Explainability requirements: Regulators expect you to explain decisions. The NIST AI Risk Management Framework and ISO/IEC 42001 provide guidance on responsible AI implementation. Build systems that can tell you why a transaction was flagged, not just that it was.

False positive investigation: Set up workflows to investigate and label false positives. These become your highest-quality training data for the next model iteration.

A/B testing: Before deploying a new model to all customers, test it against a subset. Measure both fraud reduction and false positive impact before full rollout.

Balancing Fraud Prevention with Customer Experience

Here's the uncomfortable truth: you can't eliminate fraud without impacting customer experience. The goal is optimization, not perfection.

Some institutions handle this by adding a secondary verification step for high-risk transactions instead of blocking them outright. A customer gets prompted to authenticate (via biometric, one-time code, etc.) rather than having their legitimate transaction declined.

This approach:

Catches genuine fraud (fraudsters usually can't complete the secondary step)

Preserves customer experience for legitimate users (they're asked to verify, not denied)

Gives you better data (you learn whether the transaction was actually fraudulent)

Compliance and Regulatory Considerations

Real-time fraud detection intersects with multiple regulatory frameworks:

Strong Customer Authentication (SCA) requirements under PSD2 and similar regulations mandate specific verification approaches for certain transaction types. Ensure your fraud detection system works within these constraints, not against them.

Fair lending and bias concerns: AI models can inadvertently encode bias if trained on biased data. Audit your model for disparate impact across demographic groups. This is both a regulatory requirement and a fairness issue. The Partnership on AI provides resources on responsible AI implementation.

Documentation and auditability: Regulators expect clear documentation of your model design, training data, performance metrics, and decision logic. Build this documentation from day one, not as an afterthought.

Conclusion

AI-driven fraud detection isn't a magic solution—it's a tool that requires thoughtful implementation. The institutions winning with real-time payments aren't the ones with the most sophisticated models; they're the ones who've aligned fraud detection with business outcomes, customer experience, and regulatory requirements.

Start with clean data and simple models. Monitor performance obsessively. Calibrate thresholds to your specific cost structure. Iterate based on real-world performance.

The balance between catching fraud and preserving customer experience isn't static. As your fraud patterns evolve, your detection system needs to evolve with them.

Ready to Deploy AI-Driven Fraud Detection at Scale?

CatalystX helps financial institutions implement real-time fraud detection systems that catch threats without frustrating legitimate customers. From fraud model design to production deployment and continuous monitoring, we provide the expertise and platform to build fraud detection that actually works.

.png)

.svg)