Agentic AI in Lending: From Pilot to Production

70% of banks pilot agentic AI in lending but fewer than 20% deploy it. Here is the governance framework fintech leaders need to move safely into live operation.

70% of banks pilot agentic AI in lending but fewer than 20% deploy it. Here is the governance framework fintech leaders need to move safely into live operation.

Subscribe now for best practices, research reports, and more.

Most financial institutions running agentic AI pilots in lending already know the technology works. The model performs in testing. The business case is clear. The internal presentation goes well. And then the risk committee asks one question that stops everything: if this AI declines a borrower's application, can we explain exactly why in terms a regulator will accept?

That single question is why 70% of banks are running agentic AI pilots but fewer than 20% have crossed into live production. The gap is not a technology problem. It is a governance, architecture, and risk management problem, and every quarter an institution remains inside it carries a measurable cost.

This article is for fintech leaders, technology executives, product heads, and risk professionals who want to understand what separates institutions that have crossed from pilot to production from the majority that have not, and what it takes to close that gap responsibly.

McKinsey research on banking automation demonstrates that institutions deploying AI across document processing and credit decisioning achieve cost savings exceeding 30% in targeted functions, with advanced deployments reducing cost per originated loan by 20 to 40%.

The manual time embedded in a standard lending workflow illustrates why:

Agentic AI automates the majority of these steps, compresses end-to-end processing from days to hours, and reserves human involvement for genuine judgement cases. The competitive pressure is real: borrowers who receive decisions within hours from digital-native lenders are increasingly unwilling to wait the multi-day timelines that manual processes produce.

One: No Explainability Layer

Under the EU AI Act's high-risk AI system classifications, which entered enforcement in August 2026, algorithmic explainability in lending is a legal requirement. What this demands in practice:

This is an architecture decision. Explainability must be built in from the outset, not retrofitted after deployment.

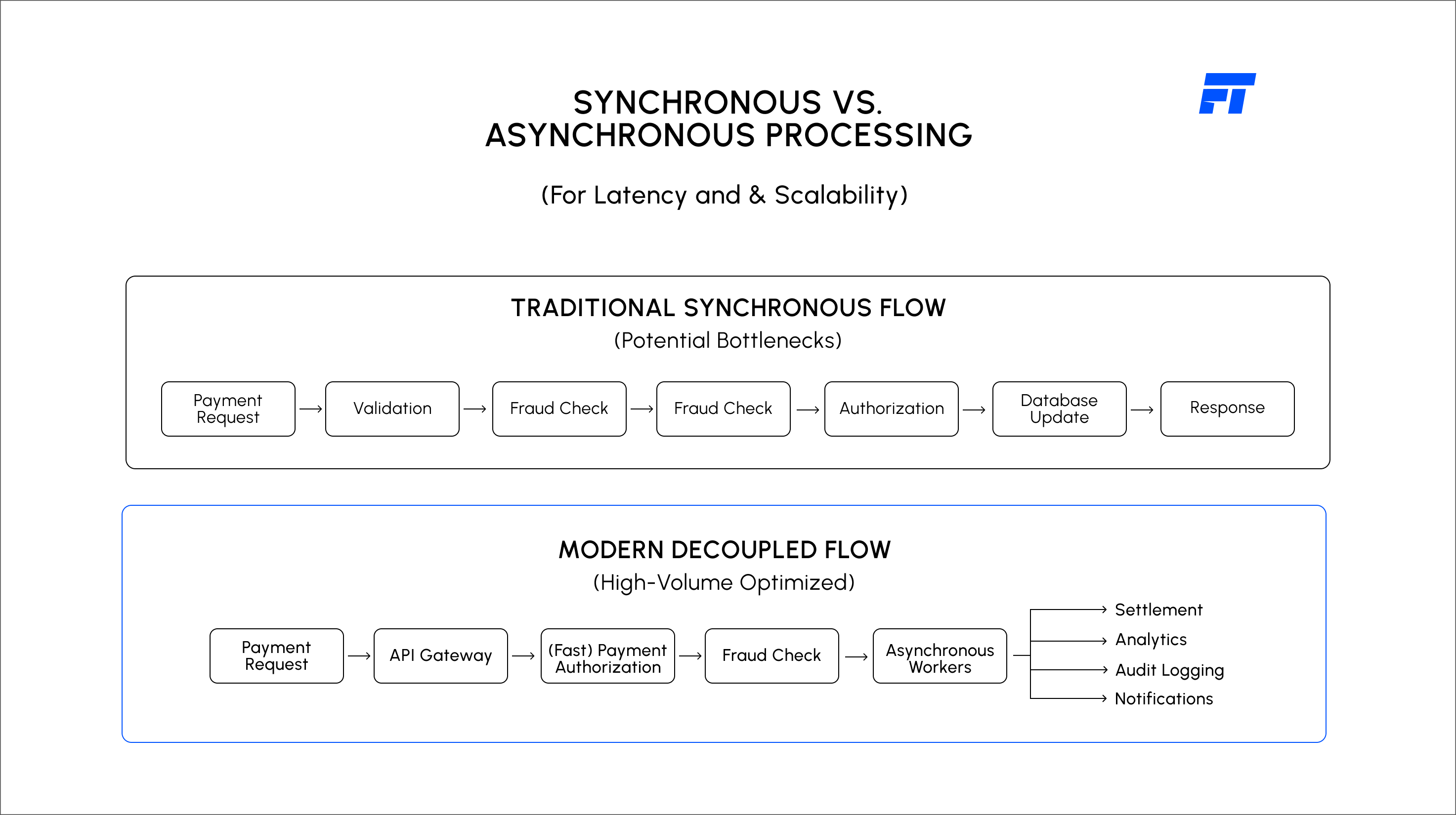

Two: No Human Override at Escalation Points

Every successful production deployment shares the same design pattern:

Without this structure, automated decisions carry regulatory liability that the governance framework cannot defend.

The most common reason pilots fail in the move to production is infrastructure, not model performance. The specific gaps that block deployment:

Production deployment requires a middleware orchestration layer connecting every component into a coherent, live data environment.

FyscalTech's Catalyst X integration platform provides the connective layer that production deployment requires.

Before any agentic lending AI moves into live operation, the following conditions must be confirmed:

This is the minimum viable governance standard for responsible agentic AI deployment in a regulated lending environment.

Accenture's research on next-generation lending identifies consistent outcomes within twelve months of production deployment:

The competitive gap between institutions in production and those still in pilot mode widens every quarter. The institutions that have crossed over are building model maturity on live data. Those still testing are not.

The gap between pilot and production is not a technology gap. It is a governance and architecture gap. The institutions closing it fastest are not those with the most sophisticated AI research capability. They are those that treated explainability, human oversight, and real-time integration as design requirements from the beginning rather than as problems to solve after deployment.

For fintech leaders evaluating this decision, the question is no longer whether agentic AI in lending is ready. It is whether your governance infrastructure is.

FyscalTech's Lending AI Suite, including the NOVA origination agent and GreyCells credit intelligence layer, is built for production deployment on existing infrastructure without wholesale system replacement.

.png)

.svg)

.svg)

.svg)

.svg)